Cryptocurrencies can be risky investments. Please do your own research before investing. Our content may contain affiliate links. Read our disclosures:

Nexo is a digital assets wealth platform that offers crypto-backed lending, high-yield savings accounts, a built-in exchange, a dual-mode debit and credit card, and perpetual futures trading under one roof. Founded in 2018, Nexo introduced the first instant crypto-backed credit line and has since grown to serve over 7 million clients across more than 150 jurisdictions, with $11 billion or more in assets under management as of September 2025.

In this comprehensive Nexo review for 2026, we break down everything that matters: current interest rates by loyalty tier, how borrowing works in practice, the Nexo Card's cashback structure, the platform's seven security certifications, its regulatory licenses across multiple countries, the NEXO token's utility, and where the platform falls short. We have used the platform, studied the latest rate changes from November 2025, and compared Nexo against every meaningful CeFi alternative still operating.

Our verdict: 4.2 / 5 — Nexo is the strongest all-in-one centralized finance platform available in 2026 for crypto holders who want to earn yield, borrow against holdings, trade, and spend without selling. The $5,000 minimum portfolio balance and NEXO token requirement for top-tier rates are real friction points, but no competitor matches the combination of feature depth, security infrastructure, and operational track record that Nexo delivers.

Last updated: February 11, 2026

| Category | Rating |

|---|---|

| Fees & Pricing | ⭐⭐⭐⭐ (4/5) |

| Security | ⭐⭐⭐⭐⭐ (5/5) |

| Ease of Use | ⭐⭐⭐⭐ (4/5) |

| Crypto Selection | ⭐⭐⭐⭐ (4/5) |

| Staking/Rewards | ⭐⭐⭐⭐½ (4.5/5) |

| Customer Support | ⭐⭐⭐½ (3.5/5) |

| Feature | Details |

|---|---|

| Founded | 2018 (Zug, Switzerland) |

| Assets Under Management | $11+ billion (as of September 2025) |

| Registered Users | 7+ million |

| Supported Assets | 100+ cryptocurrencies, stablecoins, and fiat |

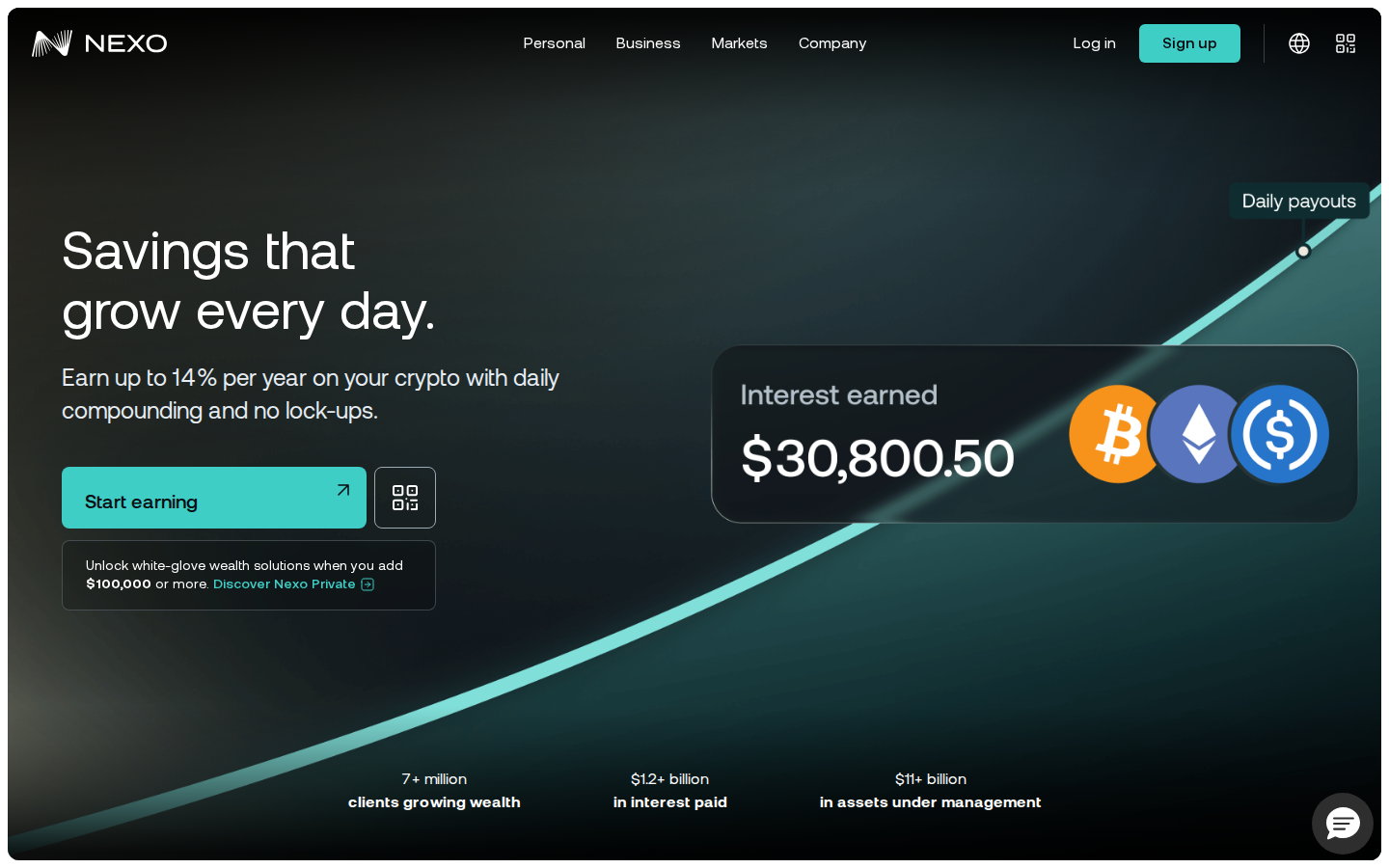

| Max Flexible Earn Rate | Up to 14% APY (stablecoins, Platinum tier) |

| Max Fixed-Term Earn Rate | Up to 16% APY (stablecoins, Platinum tier) |

| Lowest Borrow Rate | From 2.9% APR (Platinum tier) |

| Nexo Card Cashback | Up to 2% in crypto |

| Minimum Portfolio Balance | $5,000 to earn interest |

| Minimum Earning Balance per Asset | $500 equivalent (since November 2025) |

| Trustpilot Rating | 4.4 out of 5 (Excellent) |

| Interest Paid to Date | $1.2+ billion |

| Transaction Volume Processed | $371+ billion |

| Jurisdictions | 150+ |

| Security Certifications | SOC 2 Type 2, SOC 3, ISO 27001, ISO 27017, ISO 27018, CSA STAR Level 1, CCSS Level 3 |

| US Availability | Re-entered April 2025; lending and borrowing available, earn features limited by state |

Who Is Nexo Best For?

Nexo is best suited for long-term crypto holders who want their assets generating returns rather than sitting idle. The platform's strength lies in combining multiple financial services -- earning, borrowing, trading, and spending -- into a single interface. Specifically, Nexo works well for:

- Yield seekers who want to earn up to 16% APY on stablecoins or up to 8% on Bitcoin and Ethereum through fixed-term savings

- Tax-conscious investors who prefer borrowing against their crypto rather than selling and triggering taxable events

- Daily spenders who want to use a crypto-linked Mastercard with up to 2% cashback without liquidating holdings

- High-net-worth individuals who can access Nexo Private for credit lines up to $200 million, 0% interest custom solutions, and a dedicated relationship manager

- Institutional clients looking for OTC trading, bespoke custody, and enterprise-grade infrastructure

Nexo is not ideal for users with portfolios under $5,000, as the minimum balance requirement locks them out of the earn program entirely. It is also not suitable for users who refuse to hold NEXO tokens, since top-tier rates require 10% of your portfolio in the native token.

How the Nexo Loyalty Program Works

The Nexo loyalty program is the backbone of the platform's pricing structure. Every rate, fee, and benefit is tied to your loyalty tier, which is determined by the percentage of NEXO tokens you hold relative to your total portfolio balance. There are four tiers: Base, Silver, Gold, and Platinum.

| Benefit | Base (less than 1% NEXO) | Silver (1%+ NEXO) | Gold (5%+ NEXO) | Platinum (10%+ NEXO) |

|---|---|---|---|---|

| NEXO Token Ratio Required | Less than 1% | 1% or more | 5% or more | 10% or more |

| Borrow APR (Best Available) | 18.9% | 17.9% | 13.9% | 2.9% |

| Flexible Earn on Stablecoins (In-Kind) | Up to 8% | Up to 9% | Up to 11% | Up to 12% |

| Fixed-Term Earn on Stablecoins (In-Kind) | Up to 10% | Up to 11% | Up to 13% | Up to 14% |

| Flexible Earn on BTC (In-Kind) | Up to 1% | Up to 1.5% | Up to 2.5% | Up to 3.5% |

| Fixed-Term Earn on BTC (In-Kind) | Up to 2% | Up to 2.5% | Up to 3.5% | Up to 4.5% |

| Exchange Cashback | None | 0.1% | 0.25% | 0.5% |

| Nexo Card Cashback | 0.5% | 1% | 1.5% | 2% |

| Free Crypto Withdrawals per Month | 0 | 0 | 0 | 1 on BTC/ETH/TIA/BSC networks; unlimited on 15+ other networks |

| Free Bank Transfer per Month | 0 | 0 | 0 | 1 |

| Physical Nexo Card | No | No | Yes | Yes |

The tier system rewards commitment to the Nexo ecosystem. Holding 10% of your portfolio in NEXO tokens to reach Platinum unlocks dramatically better rates across every product. The gap between Base (18.9% borrow APR) and Platinum (2.9% borrow APR) is massive, making the NEXO token essentially a required purchase for serious users.

Nexo Earn: Interest Rates by Asset and Tier

Nexo's earn program is one of the highest-yielding CeFi offerings available in 2026. Interest is paid daily with automatic compounding, and users can choose between Flexible Savings (no lock-up, withdraw anytime) and Fixed-Term Savings (higher rates with 1, 3, or 12-month lock periods). As of the November 24, 2025 rate update, here are the current rates:

| Asset | Savings Type | Base | Silver | Gold | Platinum |

|---|---|---|---|---|---|

| Bitcoin (BTC) | Flexible | Up to 1% | Up to 1.5% | Up to 2.5% | Up to 3.5% |

| Bitcoin (BTC) | Fixed (1 month) | Up to 2% | Up to 2.5% | Up to 3.5% | Up to 4.5% |

| Ethereum (ETH) | Flexible | Up to 2% | Up to 2.5% | Up to 4% | Up to 5% |

| Ethereum (ETH) | Fixed (1 month) | Up to 3% | Up to 3.5% | Up to 5% | Up to 6% |

| USDC / USDT (Stablecoins) | Flexible | Up to 8% | Up to 9% | Up to 11% | Up to 12% |

| USDC / USDT (Stablecoins) | Fixed (3 months) | Up to 10% | Up to 11% | Up to 13% | Up to 14% |

| NEXO Token | Flexible | Up to 3% | Up to 4% | Up to 6% | Up to 7% |

| NEXO Token | Fixed (3-12 months) | Up to 6% | Up to 7% | Up to 9% | Up to 9% |

| Solana (SOL) | Flexible | Up to 3% | Up to 3.5% | Up to 5% | Up to 6% |

| XRP | Flexible | Up to 2% | Up to 2.5% | Up to 4% | Up to 5% |

| EUR / USD / GBP (FIATx) | Flexible | Up to 4% | Up to 5% | Up to 7% | Up to 8% |

Key details about Nexo Earn:

- Interest compounds daily and is paid out every 24 hours

- A minimum portfolio balance of $5,000 across your entire Nexo account is required to earn any interest

- Since November 2025, each individual asset requires a minimum balance of $500 equivalent to earn interest

- Fixed-term lock periods are 1 month for cryptocurrencies, 3 months for stablecoins, and 3 to 12 months for fiat and NEXO tokens

- Assets locked in fixed terms can still be used as collateral for borrowing or Nexo Card spending

- Rates shown are "up to" figures -- larger balances above $4 million may earn reduced rates on the excess portion

- Earning in NEXO tokens instead of in-kind previously offered a bonus, but as of recent updates, in-kind earning is the standard for most assets

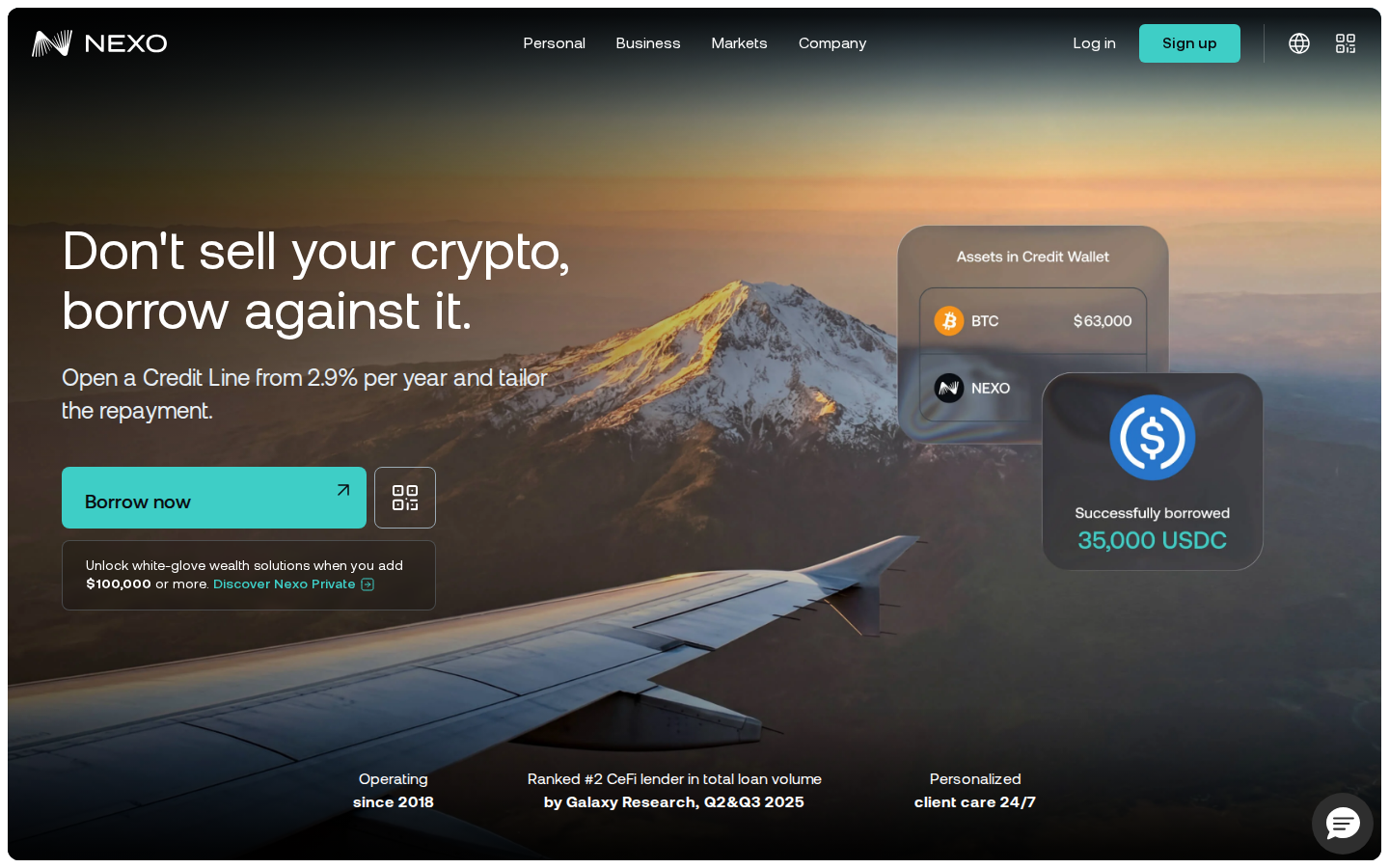

Nexo Borrow: Crypto-Backed Credit Lines

Nexo's crypto-backed credit line is the platform's founding product and remains one of its strongest offerings. It allows you to borrow between $50 and $2 million instantly against your crypto holdings, with no credit checks, no fixed repayment schedule, and no origination fees. For private clients with over $100,000 in digital assets, credit lines of up to $200 million are available with dedicated relationship management.

Borrowing on Nexo works through an over-collateralization model. Each supported asset has a specific loan-to-value (LTV) ratio that determines how much you can borrow against it. If your collateral's value drops and the LTV rises too high, Nexo automatically transfers assets from your Savings Wallet to your Credit Wallet to maintain the loan's health. If the LTV continues to rise, partial liquidation may occur.

| Feature | Details |

|---|---|

| Borrow Range | $50 to $2 million (up to $200M for private clients) |

| BTC Loan-to-Value | 50% (borrow up to half the value of your Bitcoin) |

| ETH Loan-to-Value | 50% |

| Stablecoin LTV | Up to 90% |

| Altcoin LTV | 15% to 40% (varies by asset) |

| Borrow APR (Platinum) | From 2.9% |

| Borrow APR (Gold) | From 5.9% |

| Borrow APR (Silver) | From 8.9% |

| Borrow APR (Base, $5,000+ portfolio) | From 13.9% |

| Borrow APR (Under $5,000 portfolio) | 18.9% |

| Credit Check Required | No |

| Origination Fee | None |

| Repayment Schedule | Flexible -- repay anytime, no minimum installments |

| Repayment Currency | Crypto, stablecoins, FIATx, or a combination |

| Early Repayment | Allowed; note that loans repaid within 45 days may incur early repayment costs |

| Multi-Asset Collateral | Yes -- combine 100+ supported assets |

| Output Options | Stablecoins to Nexo account or fiat to bank account |

The borrowing experience is genuinely seamless. Once your account is verified and assets are deposited, you can open a credit line in under a minute. There is no approval queue, no paperwork, and no waiting period. The tax advantage is significant: borrowing against crypto avoids the taxable event that selling would trigger, which makes Nexo's credit line popular among long-term holders who need liquidity without exiting their positions.

Nexo Booster

For users seeking leveraged exposure, Nexo Booster allows you to use your existing holdings as collateral to acquire 1.5x to 3x more of the same or another digital asset. The additional purchase is financed through a credit line, and the total position has a maximum LTV of 70%. Nexo provides take-profit and stop-loss tools for risk management, but the product carries significant risk and is intended for experienced users who understand leverage.

Nexo Card: Spend Crypto Without Selling

The Nexo Card is a Mastercard-branded payment card that lets you spend your crypto or borrow against it at the point of purchase. It is one of the most feature-rich crypto cards available because it offers two distinct modes:

- Debit Mode: Directly sells your fiat, stablecoin, or crypto balance to fund the purchase. Assets continue earning interest in Flexible Savings until the moment they are spent. You earn up to 2% cashback in crypto (BTC, NEXO, or other supported assets).

- Credit Mode: Does not sell your assets. Instead, each purchase draws from your available credit line, using your crypto portfolio as collateral. You keep your market exposure while spending. Cashback rates also apply in credit mode.

The card is accepted at over 100 million merchants worldwide and is currently available in more than 30 countries, with plans for broader rollout. Cashback rates are tied to your loyalty tier: 0.5% at Base, 1% at Silver, 1.5% at Gold, and 2% at Platinum. Physical cards are available only for Gold and Platinum tier members.

Nexo Card fees: Processing fees range from 1.99% for EEA countries to 3.49% for non-EEA countries. Currency conversion carries a 0.9% to 3.1% fee. ATM withdrawals incur a 2% fee after your free monthly ATM withdrawal limit.

Nexo Exchange and Trading

Nexo includes a built-in exchange that supports over 1,500 trading pairs through its Smart Routing system. The Smart Routing technology scans multiple external exchanges simultaneously to find the best available price, splitting orders across venues for optimal execution. This aggregation approach often delivers better effective rates than trading on a single exchange.

Key trading features include:

- Instant Swap: One-tap conversion between any supported assets with cashback up to 0.5% depending on loyalty tier

- Recurring Buys: Schedule automated purchases at set intervals for dollar-cost averaging strategies

- Target Price Swap: Set limit orders that execute when your specified price is reached

- Crypto Baskets: Diversify with a single tap into curated baskets like Essentials (BTC, ETH, XRP, SOL, NEXO), DeFi (AAVE, ONDO, ENA, PENDLE, MORPHO), and Memecoins (DOGE, PEPE, SHIB, BONK, TRUMP)

- OTC Swap: For trades between $250,000 and $3 million on select pairs, with competitive institutional pricing

- Perpetual Futures: 100+ contracts with up to 100x leverage, multi-asset collateral support, and risk management tools including stop-loss and take-profit orders

Swapped assets are instantly credited to your Savings Wallet and begin earning interest immediately, which is a thoughtful design that maximizes yield generation.

Nexo Security and Insurance

Nexo holds seven security certifications and attestations, making it the most certified crypto platform by a significant margin. Security is arguably Nexo's strongest differentiator against competitors, especially given the wave of CeFi platform failures in 2022 that wiped out billions in customer funds.

Certifications held by Nexo:

- SOC 2 Type 2 -- Completed for three consecutive years, audited by the American Institute of Certified Public Accountants (AICPA). Validates controls over data security, availability, and confidentiality.

- SOC 3 Type 2 -- Public-facing report confirming the same standards as SOC 2, providing transparency to prospective clients.

- ISO/IEC 27001:2022 -- The international standard for information security management systems, granted by RINA.

- ISO/IEC 27017:2015 -- Cloud security controls standard.

- ISO/IEC 27018:2019 -- Protection of personally identifiable information in public cloud environments.

- CSA STAR Level 1 -- Cloud Security Alliance's Security, Trust, Assurance, and Risk registry.

- CCSS Level 3 -- The highest level of the Cryptocurrency Security Standard, audited by Deloitte. Requires multi-signature schemes, geographically distributed key storage, and advanced cryptographic safeguards.

Custody infrastructure: Nexo uses Fireblocks and Ledger Vault for institutional-grade custody. Assets are held in 100% cold storage using bank-grade Class III vaults. The platform employs multi-party computation (MPC) technology and hardware security modules to protect private keys.

Insurance: Nexo maintains custodial insurance coverage through its custody partners. The exact coverage amount has varied over time -- Nexo previously cited $775 million in insurance through BitGo and other providers. Users should verify current coverage amounts directly with Nexo, as insurance arrangements can change.

Anti-scam engine: Every withdrawal is analyzed in real time by an AI-powered anti-scam engine that detects fraudulent patterns before transactions are completed. If suspicious activity is identified, the system provides contextual warnings or temporarily pauses the action.

Note on proof of reserves: Nexo previously had real-time proof-of-reserves attestations through Armanino, but these ended in early 2023 when Armanino exited crypto auditing. As of 2026, Nexo does not offer a live, publicly verifiable proof-of-reserves dashboard. This is a legitimate criticism that the platform should address.

Regulatory Status and Licenses

Nexo is one of the most broadly licensed crypto platforms in the industry, holding registrations and licenses across multiple jurisdictions. This regulatory footprint is a key trust factor, especially for users comparing Nexo against competitors that operate without clear regulatory oversight.

Known licenses and registrations include:

- United States (California): Financing Law License from the Department of Financial Protection and Innovation (Reference No. 60DBO-109416), held by Nexo Financial LLC

- Australia: Digital Currency Exchange Provider registration with AUSTRAC (Reference No. DCE100843695-001), held by Nexo Australia Pty Ltd

- Hong Kong: Trust or Company Service Provider License from the Companies Registry (Reference No. TC007556), held by Nexo Finance Limited

- Poland: Registration of Activities in the Field of Virtual Currencies with the Ministry of Finance (Reference No. RDWW-533), held by Nexo Services Sp. z o.o.

- Seychelles: Securities Dealer License from the Financial Services Authority (Reference No. SD121), held by Nexo Markets Ltd

US market re-entry: Nexo officially re-entered the United States on April 28, 2025, after previously withdrawing from the US market due to regulatory challenges. The re-entry was announced at a business event featuring keynote addresses from Donald Trump Jr. and Nexo Co-Founder Antoni Trenchev. US clients now have access to lending and borrowing features, though earning interest on deposits remains restricted in certain states due to varying state-level regulations.

Compliance partners: Nexo works with Chainalysis for blockchain analytics, Jumio and SumSub for KYC and identity verification, Sift for fraud detection, and Unit21 for anti-money-laundering monitoring. The platform is also a member of the Association of Certified Sanctions Specialists (ACSS) and the Merchant Risk Council (MRC).

NEXO Token Utility and Tokenomics

The NEXO token is an ERC-20 token built on the Ethereum blockchain with a total supply of 1 billion tokens. It serves as the utility token powering the entire loyalty program and is essential for unlocking the best rates on the platform. As of early 2026, NEXO has a fully diluted market cap of approximately $1.2 billion, placing it in the top 100 cryptocurrencies by market capitalization.

NEXO token benefits include:

- Determines your loyalty tier (1%, 5%, or 10% of portfolio in NEXO for Silver, Gold, Platinum respectively)

- Earns interest of up to 9% APY through fixed-term savings

- Unlocks lower borrowing rates (down to 2.9% APR at Platinum)

- Provides higher cashback on the Nexo Card and exchange swaps

- Grants free withdrawals at higher tiers

- Can be used as collateral for borrowing

The NEXO token creates a meaningful incentive loop: the more you hold, the better your rates become across every product. However, this also introduces concentration risk -- users must hold a meaningful percentage of their portfolio in a single asset to access the best terms, which may not suit conservative investors.

Nexo Fees and Costs

| Fee Type | Amount |

|---|---|

| Account Opening | Free |

| Account Maintenance | Free |

| Crypto Deposits | Free |

| Fiat Deposits (Bank Transfer) | Varies by method -- fees may apply for incoming bank transfers |

| Fiat Deposits (Card) | Visa, Mastercard, Apple Pay, Google Pay supported -- card processing fees may apply |

| Crypto Withdrawals | Network fee only (Platinum: 1 free BTC/ETH/TIA/BSC withdrawal per month; unlimited free on 15+ networks) |

| Fiat Withdrawals (SEPA) | 5 EUR (Platinum: 1 free per month) |

| Fiat Withdrawals (Faster Payments) | 5 GBP (Platinum: 1 free per month) |

| Fiat Withdrawals (ACH) | 10 USD |

| Fiat Withdrawals (SWIFT) | 25 EUR / 25 GBP / 25 USD |

| Exchange Spread | Approximately 0.5% (varies by pair and volume) |

| Loan Origination | Free |

| Loan Interest (Platinum) | From 2.9% APR |

| Early Loan Repayment | Costs may apply if repaid within 45 days |

| Nexo Card Processing (EEA) | 1.99% |

| Nexo Card Processing (Non-EEA) | 3.49% |

| Nexo Card Currency Conversion | 0.9% to 3.1% |

| ATM Withdrawal | 2% after free monthly limit |

Nexo Private: Wealth Solutions for High-Net-Worth Clients

Nexo Private is a white-glove service for clients with over $100,000 in digital assets. It provides access to credit lines of up to $200 million, custom credit solutions with 0% annual interest, a dedicated relationship manager, prioritized client care, and bespoke portfolio strategies. For high-net-worth individuals, family offices, and institutions, Nexo Private represents one of the few institutional-grade CeFi offerings with a meaningful track record.

Nexo Dual Investment

Nexo's Dual Investment product targets higher returns through structured buy-low or sell-high strategies on assets like BTC, ETH, and XRP. Users deposit a supported asset, choose a target price and settlement date. If the target is reached, the asset converts to the settlement currency with enhanced yield. If not, the original asset is returned with interest. This product carries meaningful market risk and is designed for users comfortable with volatility.

Nexo Ventures

Nexo Ventures is the company's investment arm focused on funding early-stage blockchain and digital infrastructure projects. The team provides startups with capital, mentorship, and access to Nexo's global network. This allows Nexo to maintain visibility into emerging trends while supporting the broader digital asset ecosystem.

User Experience and Mobile App

Nexo offers a clean, intuitive interface across web, iOS, Android, and Huawei devices. Account creation takes minutes, and KYC verification typically completes in under 10 minutes through automated ID checks. The mobile app provides the full feature set available on web, including earning, borrowing, exchange, card management, and futures trading.

The platform maintains 24/7 client care through live chat (with an AI assistant) and email support. There is also an extensive help center with educational articles and guides. The Nexo app holds a 4-star rating with thousands of reviews on both the Google Play Store and Apple App Store, with users praising speed and functionality.

Notable UX features include real-time portfolio analytics, customizable alerts for market movements and account activity, biometric login, address whitelisting, anti-phishing codes for verifying official communications, and automated tax reporting through a Koinly integration.

Nexo vs Competitors: How Does It Compare?

The CeFi lending landscape has contracted significantly since 2022, with Celsius, BlockFi, and Voyager all going bankrupt. The remaining alternatives each have specific strengths but none match Nexo's breadth. Here is how Nexo compares against the surviving competitors:

| Feature | Nexo | YouHodler | Ledn | CoinLoan |

|---|---|---|---|---|

| Founded | 2018 | 2018 | 2018 | 2017 |

| AUM | $11B+ | Not disclosed | $1B+ (reported) | Not disclosed |

| Supported Assets | 100+ | 75+ | BTC, ETH, USDC, USDT | 20+ |

| Max Stablecoin Earn Rate | Up to 14% (fixed) | Up to 12% | Up to 10% | Up to 10% |

| Max BTC Earn Rate | Up to 4.5% (fixed) | Up to 4.5% | Up to 3% | Up to 5% |

| Borrow APR (Best) | From 2.9% | From 3% | From 7.9% | From 4.95% |

| Payment Card | Yes (Mastercard, dual mode) | No | No | Yes (limited) |

| Built-in Exchange | Yes (1,500+ pairs) | Yes | Limited | Yes |

| Futures Trading | Yes (100+ contracts, up to 100x) | No | No | No |

| Security Certifications | 7 (SOC 2, SOC 3, ISO 27001, ISO 27017, ISO 27018, CSA STAR, CCSS L3) | Limited | SOC 2 | Limited |

| US Availability | Yes (re-entered April 2025, limited earn) | No | Yes (BTC lending) | No |

| Proof of Reserves | No (ended 2023) | No | Yes (Armanino) | No |

| Mobile App | iOS, Android, Huawei | iOS, Android | iOS, Android | iOS, Android |

| Jurisdictions | 150+ | Undisclosed | 130+ | EU-focused |

Note on Celsius: Celsius Network filed for bankruptcy in July 2022, owing approximately $4.7 billion to creditors. It is no longer operational. If you previously used Celsius, Nexo and the alternatives above represent the strongest remaining options for crypto lending.

What Nexo Does Well

- Comprehensive product suite: No other CeFi platform combines earn, borrow, exchange, futures, card, and institutional services under one roof at this scale

- Industry-leading security: Seven certifications including SOC 2 Type 2, ISO 27001, and CCSS Level 3 from Deloitte. This is unmatched in the crypto industry

- Competitive earn rates: Up to 14% on stablecoins (flexible) and 16% on fixed terms at Platinum tier outperform most competitors

- Flexible borrowing: No credit checks, no fixed schedule, multi-asset collateral, and rates from 2.9% APR

- Dual-mode card: The ability to switch between debit and credit mode on a single Mastercard is unique in crypto

- Track record: Survived the 2022 CeFi collapse that killed Celsius, BlockFi, and Voyager. Ranked as the second-largest centralized crypto lender in 2025 by Galaxy Research

- Daily interest compounding: Interest paid every 24 hours rather than weekly or monthly maximizes compound growth

- Tax reporting integration: Koinly partnership simplifies tax compliance

Where Nexo Falls Short

- $5,000 minimum portfolio balance: Users with smaller portfolios cannot earn any interest, which effectively excludes beginners and casual users

- $500 minimum per asset (since November 2025): You need at least $500 worth of each individual asset to earn interest on it, adding another barrier

- NEXO token dependency: Top-tier rates require holding 10% of your portfolio in NEXO tokens. This introduces concentration risk and feels like a forced buy

- No proof of reserves: Nexo's Armanino attestation ended in early 2023, and no replacement has been implemented. This is a gap in transparency

- Centralized custody risk: All assets are held by Nexo. While their security infrastructure is strong, CeFi platforms carry inherent counterparty risk

- Limited US earning features: While Nexo re-entered the US, earning interest is restricted in certain states

- Card fees for non-EEA users: The 3.49% processing fee for non-EEA countries and up to 3.1% currency conversion significantly erode the 2% cashback benefit

- Rates are "up to" figures: Actual rates depend on tier, asset, balance size, and market conditions. Large balances above $4 million earn reduced rates on the excess

Recent Developments in 2025 and 2026

- April 2025: Nexo officially re-entered the US market, making lending and borrowing available to American clients

- Q2-Q3 2025: Ranked as the second-largest centralized crypto lender by Galaxy Research, trailing only Tether

- October 2025: Announced rate adjustments effective November 24, 2025, reducing some flexible savings rates while maintaining competitive fixed-term bonus rates

- November 2025: Introduced $500 minimum earning balance per asset, replacing the previous per-asset minimum structure

- 2025: Launched Wealth Vaults, allowing users to lock Bitcoin for up to 20 years with early access if needed

- 2025: Expanded perpetual futures offering to over 100 contracts with up to 100x leverage

- 2025: Added crypto baskets for one-tap diversification across curated asset groups

- 2025: Deployed AI-powered Anti-scam Engine for real-time withdrawal fraud detection

How to Get Started with Nexo

- Create an account: Visit Nexo and register with your email address. Create a strong password.

- Complete KYC verification: Provide your legal name, country of residence, and identity documents. Most users complete verification in under 10 minutes.

- Deposit funds: Add cryptocurrency via supported blockchain networks, fiat via bank transfer (SEPA, Faster Payments, ACH, SWIFT), or purchase crypto directly with Visa, Mastercard, Apple Pay, or Google Pay.

- Opt in to earn interest: Activate the earn interest option in your account settings. Ensure your total portfolio balance is at least $5,000.

- Consider your loyalty tier: If you want the best rates, purchase NEXO tokens equal to 10% of your portfolio value to reach Platinum tier.

- Explore additional features: Open a credit line, activate your Nexo Card, set up recurring buys, or explore futures trading.

Nexo Alternatives Worth Considering

If Nexo does not fit your needs, here are the strongest alternatives for crypto lending and earning in 2026:

- YouHodler: Strong earn rates, multi-chain support, and crypto-backed loans. Best for users who want similar features without a loyalty token requirement. Not available in the US.

- Ledn: Bitcoin-focused lending platform with proof-of-reserves attestations. Best for BTC holders who prioritize transparency. Limited asset support compared to Nexo.

- CoinLoan: EU-regulated platform with competitive earn rates and borrowing. Best for European users who want a straightforward CeFi experience.

- EarnPark: Offers competitive yields across a range of assets. Worth comparing rates against Nexo for your specific holdings.

For a detailed comparison of all available platforms and live rate data, visit our crypto lending rates comparison page and crypto loan rates comparison page.

Our Review Methodology

Our Nexo review is based on hands-on testing and rigorous research conducted by the Bitcompare editorial team:

- Account testing: We created and verified a Nexo account, completing the full KYC process.

- Deposit and earn verification: We deposited funds to verify the earn program activation and interest crediting.

- Rate verification: All APY rates were cross-referenced against Nexo's official rate tables as of the November 2025 update.

- Borrowing assessment: We reviewed the credit line terms, LTV ratios, and borrowing experience.

- Security evaluation: We verified all seven security certifications through official auditor records and Nexo documentation.

- Regulatory verification: License numbers were confirmed through respective regulatory authority databases.

- Competitor comparison: We benchmarked Nexo against YouHodler, Ledn, and CoinLoan on standardised dimensions.

- Community feedback: We analysed Trustpilot reviews, app store ratings, and Reddit discussions.

Bitcompare maintains editorial independence. Our reviews are based on first-hand testing and are not influenced by partnerships. Where affiliate links are present, they do not affect our ratings or recommendations.

The Bottom Line

Nexo has earned its position as the most complete CeFi platform in crypto. Not because it is flawless -- the $5,000 minimum, NEXO token dependency for top rates, and absence of proof-of-reserves are legitimate criticisms -- but because no competitor matches its combination of feature breadth, security depth, and operational longevity.

The platform survived the 2022 CeFi apocalypse that bankrupted Celsius, BlockFi, and Voyager. It re-entered the US market. It holds seven security certifications including CCSS Level 3 audited by Deloitte. It has processed $371 billion in transaction volume and paid out over $1.2 billion in interest. Galaxy Research ranked it the second-largest centralized crypto lender in 2025, trailing only Tether.

For long-term crypto holders who want their assets working for them -- earning yield, providing liquidity through credit lines, and enabling spending without selling -- Nexo is the strongest option available in 2026. Pair it with self-custody for your cold storage holdings, and you have a robust crypto financial strategy.

Ready to put Nexo to work for you?

Nexo combines savings, borrowing, trading, and spending in a single app. Whether you are a long-term holder looking for yield, a spender who does not want to sell, or a borrower seeking tax-efficient liquidity -- Nexo delivers.

Explore Nexo NowFrequently Asked Questions

Is Nexo safe to use in 2026?

Nexo is one of the most security-certified crypto platforms in the industry, holding seven certifications: SOC 2 Type 2, SOC 3 Type 2, ISO 27001, ISO 27017, ISO 27018, CSA STAR Level 1, and CCSS Level 3 (audited by Deloitte). The platform uses Fireblocks and Ledger Vault for institutional-grade custody with 100% cold storage. Nexo survived the 2022 CeFi crisis that bankrupted Celsius, BlockFi, and Voyager, and manages over $11 billion in assets. However, as a centralized platform, it carries inherent counterparty risk, and its proof-of-reserves attestation ended in early 2023.

What interest rates does Nexo offer on crypto savings?

Nexo offers up to 14% APY on stablecoins through Flexible Savings and up to 16% through Fixed-Term Savings at the Platinum loyalty tier. Bitcoin earns up to 3.5% (flexible) or 4.5% (fixed), and Ethereum earns up to 5% (flexible) or 6% (fixed). All rates require a minimum $5,000 portfolio balance and depend on your loyalty tier, which is determined by the percentage of NEXO tokens in your portfolio.

How does Nexo borrowing work?

Nexo allows you to borrow between $50 and $2 million instantly by using your crypto as collateral, with no credit checks and no origination fees. Bitcoin and Ethereum have a 50% loan-to-value ratio, meaning you can borrow up to half their value. Interest rates start at 2.9% APR for Platinum tier members and go up to 18.9% for accounts under $5,000. Repayment is flexible with no fixed schedule.

What is the minimum balance required to earn interest on Nexo?

You need a minimum total portfolio balance of $5,000 across your Nexo account to be eligible for the earn program. Additionally, since November 2025, each individual asset requires a minimum balance equivalent to $500 to earn interest. Both Flexible and Fixed-Term Savings require meeting these thresholds independently.

How does the Nexo loyalty program work?

The Nexo loyalty program has four tiers -- Base, Silver, Gold, and Platinum -- determined by the percentage of NEXO tokens you hold relative to your total portfolio. Base is less than 1% NEXO, Silver is 1% or more, Gold is 5% or more, and Platinum is 10% or more. Higher tiers unlock better earn rates, lower borrow rates, increased card cashback, free withdrawals, and exchange cashback rewards.

Can I use Nexo in the United States?

Yes, Nexo re-entered the US market on April 28, 2025. American clients can access crypto-backed credit lines and borrowing features. However, earning interest on deposits is restricted in certain states due to varying state-level regulations. Nexo holds a Financing Law License from California's Department of Financial Protection and Innovation. Check Nexo's website for current state-by-state availability.

What is the Nexo Card and how does it work?

The Nexo Card is a Mastercard-branded payment card with two modes. In Debit Mode, it sells your crypto or fiat balance to fund purchases. In Credit Mode, it draws from your available credit line using your crypto as collateral, so you spend without selling. The card offers up to 2% cashback in crypto at the Platinum tier and is accepted at over 100 million merchants worldwide in more than 30 countries.

What fees does Nexo charge?

Nexo charges no account opening, maintenance, or deposit fees for crypto. Loan origination is free. Borrowing rates start at 2.9% APR (Platinum). Exchange spreads are approximately 0.5%. Fiat withdrawal fees range from 5 EUR (SEPA) to 25 USD (SWIFT). Platinum members get one free crypto and one free fiat withdrawal per month. The Nexo Card has a 1.99% processing fee in the EEA and 3.49% outside it.

Does Nexo have proof of reserves?

No, Nexo does not currently offer a publicly verifiable proof-of-reserves attestation. The platform previously had real-time attestations through Armanino, but these ended in early 2023 when Armanino exited crypto auditing. While Nexo's seven security certifications and $11 billion in reported AUM provide some confidence, the lack of proof-of-reserves is a notable gap in transparency compared to competitors like Ledn, which maintains Armanino attestations.

What is the NEXO token used for?

The NEXO token is an ERC-20 utility token that powers the platform's loyalty program. Holding NEXO tokens as a percentage of your portfolio determines your loyalty tier, which affects earn rates, borrow rates, card cashback, exchange cashback, and free withdrawal allowances. The token itself can earn up to 9% APY through fixed-term savings and can be used as collateral for borrowing.

How does Nexo compare to YouHodler and Ledn?

Nexo offers the broadest feature set of any CeFi platform, including earn, borrow, exchange, futures, card, and institutional services. YouHodler offers competitive earn rates and multi-chain support without requiring a loyalty token, but lacks a payment card and is not available in the US. Ledn is Bitcoin-focused with proof-of-reserves transparency and US availability, but supports far fewer assets and has no card or exchange. Nexo wins on breadth and security certifications; Ledn wins on transparency; YouHodler wins on simplicity.

Is Nexo better than a hardware wallet for storing crypto?

Nexo and hardware wallets serve different purposes. A hardware wallet like Ledger or Trezor provides self-custody where you alone control your private keys, offering maximum security against platform risk. Nexo is a custodial platform where your assets are held by the company, but they earn yield, serve as collateral for borrowing, and can be spent via card. Many users combine both: cold storage for long-term holdings they do not want to risk, and Nexo for assets they want actively working for them.